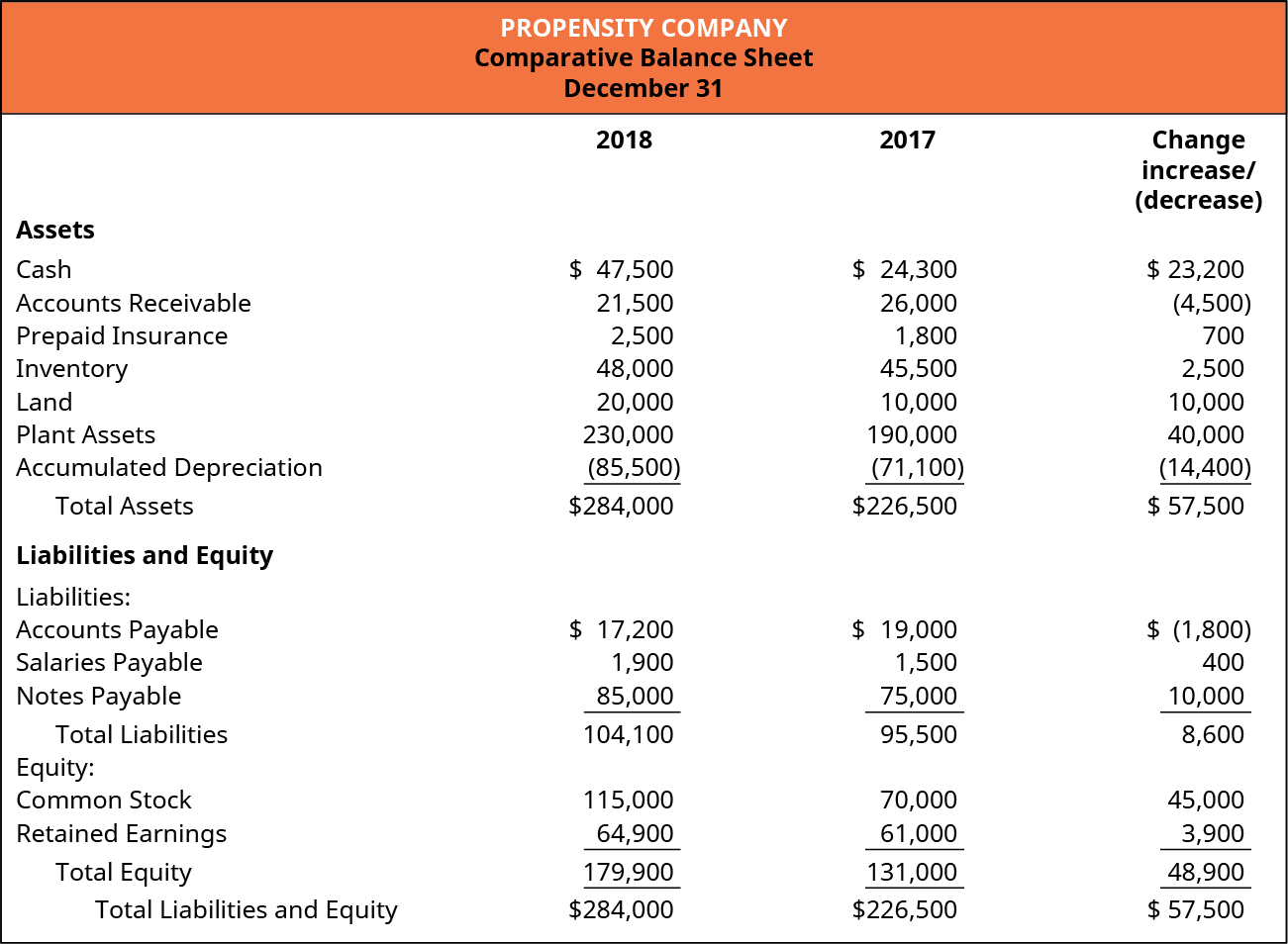

Prepare The Statement Of Cash Flows Using The Indirect Method Principles Of Accounting Volume 1 Financial Accounting

Many companies present both the interest received and interest paid as operating cash flows. Why is profit and retained earnings not included in the direct method of the cash flow statement. This article considers the statement of cash flows of which it assumes no prior knowledge. Retained earnings The amount left after paying out the dividends to the. The statement of retained earnings is a financial statement that reports the businesss net income or profit after dividends are paid out to shareholders. The amount of the adjustment -- net of tax -- is used to increase or decrease beginning retained earnings on the current retained earnings statement to arrive at adjusted beginning retained. Changes in unappropriated retained earnings usually consist of the addition of net income or deduction of net loss and the deduction of dividends and appropriations. Retained Earnings RE are the accumulated portion of a businesss profits that are not distributed as dividends to shareholders but instead are reserved for reinvestment back into the business. RE Beginning period RE Net IncomeLoss Cash Dividends Stock Dividends. Since retained earnings has no connection to net-cash flow it does not appear on the cash-flow statement that lists all changes in cash and cash equivalents for the period.

Why is profit and retained earnings not included in the direct method of the cash flow statement.

The statement of shareholders equity will include the changes in these earnings for a specific period. This article considers the statement of cash flows of which it assumes no prior knowledge. Others treat interest received as investing cash flow and interest paid as a financing cash flow. Cash flow from financing activities is one of the three categories of cash flow statements. RE Beginning period RE Net IncomeLoss Cash Dividends Stock Dividends. It is the total of profits that have been accumulated over the years for the business.

A statement of retained earnings is a formal statement showing the items causing changes in unappropriated and appropriated retained earnings during a stated period of time. Statement of cash flow. Retained earnings appear on the balance sheet as a component of owners equity. Retained earnings The amount left after paying out the dividends to the. It is the total of profits that have been accumulated over the years for the business. Profits in one period flow through the operating section of the cash flow statement on their way to the balance sheet. The method used is the choice of the finance director. Retained earnings appear on the balance sheet under shareholders equity. This statement is primarily for the use of outside parties such as investors in the firm or the firms creditors. The amount of the adjustment -- net of tax -- is used to increase or decrease beginning retained earnings on the current retained earnings statement to arrive at adjusted beginning retained.

If the loans or borrowings decrease this is due to a repayment which is an outflow of cash. Since retained earnings has no connection to net-cash flow it does not appear on the cash-flow statement that lists all changes in cash and cash equivalents for the period. This article considers the statement of cash flows of which it assumes no prior knowledge. Essentially retained cash flow is the cash provided by operating activities excluding changes in. Normally these funds are used for working capital and fixed asset purchases capital expenditures or allotted for paying off debt obligations. It is the total of profits that have been accumulated over the years for the business. Retained earnings is shown on the balance sheet under the owners equity section. But one only need to account all the receipt and payment of cash in Cash Flow Statement and any Profit or Loss from Sale of any Capital Asset will must needs to be Transferred to Capital Reserve and must be deducted from Sales Proceeds in Cash Flow Statement. Retained Earnings RE are the accumulated portion of a businesss profits that are not distributed as dividends to shareholders but instead are reserved for reinvestment back into the business. To calculate retained cash flow you need the cash flow statement from the two most recent periods.

To calculate retained cash flow you need the cash flow statement from the two most recent periods. Others treat interest received as investing cash flow and interest paid as a financing cash flow. Since retained earnings has no connection to net-cash flow it does not appear on the cash-flow statement that lists all changes in cash and cash equivalents for the period. Cash flow from financing activities is one of the three categories of cash flow statements. The statement of retained earnings is a financial statement that reports the businesss net income or profit after dividends are paid out to shareholders. Retained earnings is simply accumulated profits. The repayment of the principal is included as a cash flow from financing activities because it is the same as the repayment of a debt. See full answer below. Retained earnings appear on the balance sheet as a component of owners equity. Retained Earnings RE are the accumulated portion of a businesss profits that are not distributed as dividends to shareholders but instead are reserved for reinvestment back into the business.

This article considers the statement of cash flows of which it assumes no prior knowledge. Under IFRS there are two allowable ways of presenting interest expense in the cash flow statement. Retained earnings appear on the balance sheet as a component of owners equity. The statement of retained earnings is a financial statement that reports the businesss net income or profit after dividends are paid out to shareholders. If the loans or borrowings decrease this is due to a repayment which is an outflow of cash. These earnings can be retained and reinvested into the business. The statement of shareholders equity will include the changes in these earnings for a specific period. Since retained earnings has no connection to net-cash flow it does not appear on the cash-flow statement that lists all changes in cash and cash equivalents for the period. Why is profit and retained earnings not included in the direct method of the cash flow statement. Statement of cash flow.

Others treat interest received as investing cash flow and interest paid as a financing cash flow. Changes in unappropriated retained earnings usually consist of the addition of net income or deduction of net loss and the deduction of dividends and appropriations. But one only need to account all the receipt and payment of cash in Cash Flow Statement and any Profit or Loss from Sale of any Capital Asset will must needs to be Transferred to Capital Reserve and must be deducted from Sales Proceeds in Cash Flow Statement. Generally a large amount of retained earnings is regarded as a sign that the company has done well and is reinvesting its profits in itself. The method used is the choice of the finance director. Retained Earnings RE are the accumulated portion of a businesss profits that are not distributed as dividends to shareholders but instead are reserved for reinvestment back into the business. Calculate the retained earnings balance at the end of the period. Retained earnings is simply accumulated profits. Why is profit and retained earnings not included in the direct method of the cash flow statement. Retained earnings is shown on the balance sheet under the owners equity section.