Ace Trade Receivables In Trial Balance P And L Report Example

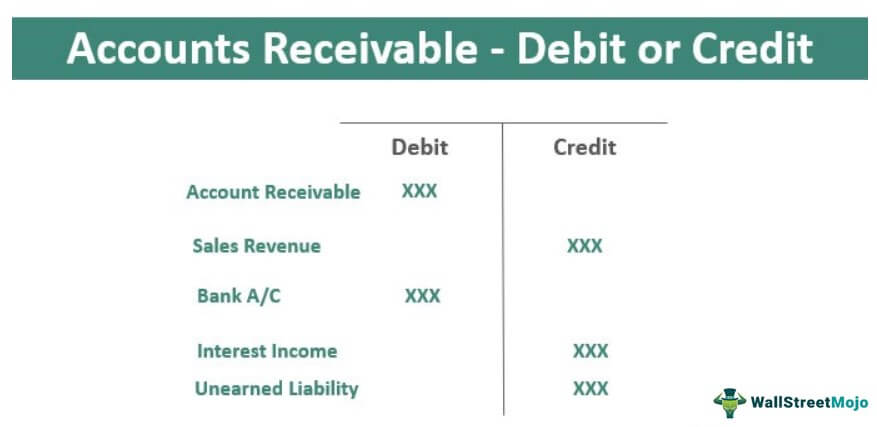

Accounts Receivable Debit Or Credit Top Examples Treatment In Ifrs

For example A Ltd sold goods to B Ltd. The accounts reflected on a trial balance are related to all major accounting. Illustrate the process of adjusting the financial statements for accruals and prepayments depreciation irrecoverable debts and the allowance for receivables. The descriptionin the trial balance is sales ledger control account debit balance on the leftand purchases ledger control account credit balance on the right. From trial balance to financial statements. 1 when I have Receivables and IRR in the Trial Balance Receivables in SFP is calculated as Receivables New Allowance Rec. The balance on the accounts receivable control account at any time reflects the amount outstanding and due to the business by customers for credit sales. The trade receivables figure will depend on the following. Once you know that you can move forward. These billings are typically documented on formal invoices which are summarized in an accounts receivable aging report.

The descriptionin the trial balance is sales ledger control account debit balance on the leftand purchases ledger control account credit balance on the right.

In the cash conversion cycle companies match the payment dates with accounts receivables making sure that receipts are made before making the payments to the suppliers. They are treated as an asset to the company and can be found on the balance sheet. An accounts receivable trial balance is an accounting tool used to total up all of the credits and debits pertaining to a companys accounts receivables. Let us say that the allowance is to be increased to 5400. Trade receivables These include all money owed to you as a direct result of the goods or services you provided hence the name trade. Once the customer has paid.

You can do this by going to AccountsCompany Data AuditorTransaction Review. Amounting to 5000. Illustrate the process of adjusting the financial statements for accruals and prepayments depreciation irrecoverable debts and the allowance for receivables. Let us say that the allowance is to be increased to 5400. These billings are typically documented on formal invoices which are summarized in an accounts receivable aging report. Once you know that you can move forward. Trade receivables arise due to credit sales. Trade receivables 180000 4000 176000 The figures in brackets are a working not part of the statement of financial position. In the cash conversion cycle companies match the payment dates with accounts receivables making sure that receipts are made before making the payments to the suppliers. Continuing the example it is more likely that the question will require the allowance to be adjusted.

To find what is causing your out of balance with Trade Debtors and Aged Receivables Id recommend running the Company Data Auditor. Accounts Receivable in Trial Balance and Balance Sheet. The value of credit sales. Amounting to 5000. Remember a JE or bank entry only affects the GL not the subledger and this will definitely cause an issue. In simple words trade receivable is the accounting entry in the balance sheet of an entity which arises due to the selling of the goods and services on credit. The period of credit given. It reflects that the company is able to realize the cash in good fashion. This help article Receivables payables or inventory out of balance has information on what can cause your issue and how to fix it. 1 when I have Receivables and IRR in the Trial Balance Receivables in SFP is calculated as Receivables New Allowance Rec.

Continuing the example it is more likely that the question will require the allowance to be adjusted. This isillustrated in the following diagram. A trial balance is a report that lists the balances of all general ledger accounts of a company at a certain point in time. Remember a JE or bank entry only affects the GL not the subledger and this will definitely cause an issue. Trade receivables 5000 Drawings 500 Cash 12200 Total 27200 24200 3000 The business has made a profit of 2000 5000 - 3000. Trade receivables consist of Debtors and Bills Receivables. Lower the accounts payable days the better. From trial balance to financial statements. The greater the value of credit sales then other things being equal the greater the total of trade receivables. Upon completion of this chapter you will be able to.

Accounts Receivable in Trial Balance and Balance Sheet. Trade receivables 5000 Drawings 500 Cash 12200 Total 27200 24200 3000 The business has made a profit of 2000 5000 - 3000. It reflects that the company is able to realize the cash in good fashion. The value of credit sales. These billings are typically documented on formal invoices which are summarized in an accounts receivable aging report. They are treated as an asset to the company and can be found on the balance sheet. Therefore the total profit now stands at 4700. Types of Assets Common types of assets include current non-current physical intangible operating and non-operating. For example A Ltd sold goods to B Ltd. The greater the value of credit sales then other things being equal the greater the total of trade receivables.

This will involve adjusting for the following items. A quick glance at the GL trial balance for the control accounts to look for Journal Entries or entries made in Bank Rec that affect the receivables control account. The balance on the accounts receivable control account at any time reflects the amount outstanding and due to the business by customers for credit sales. Receivables IRR New Allowance Rec. The value of credit sales. In this chapter we will bring together the material from theprevious chapters and produce a set of financial statements from a trialbalance. Accounts Receivable in Trial Balance and Balance Sheet. You can do this by going to AccountsCompany Data AuditorTransaction Review. Upon completion of this chapter you will be able to. The allowance for receivables is typically titled Allowance for Doubtful Accounts or Allowance for Bad Debt and has a credit balance and is considered a contra-asset because this balance offsets the debit balance in Accounts Receivable where the net result is reported as Accounts Receivable net in the balance.