Supreme Input Vat In Balance Sheet Loss And Profit

Vat Meaning

On the VAT return the 12400 input VAT should be deducted from the 30000 output VAT which in this case amounts to 17600 VAT due to HMRC. Compute in put tax from purchases made during the period get it from purchase invoices and compute the total Input VAT. Cash Flow of Funds Flow. VAT on Sales and Purchases can be adjusted against each other and if VAT on Purchase is more than VAT on sales during that month it will appear as Input VAT Credit under Current Assets Loans Advances if VAT on Sales is more than VAT on Purchases it will appear as VAT Payable under Current Liabilities Provisions in the Balance Sheet. Why Input Tax is an Asset. It is a temporary asset account like input VAT and is used to refer to prior-period purchases with VAT. Like any other outward payment VAT is. The VAT on Transactions Account - This account will usually show a credit the VAT Authorities are entitled to receive the VAT from you that you have collected from them. If you are buying or selling the Good which are under VAT you have to. At the end of every VAT period if the Output VAT will exceed the Input VAT there will be creditor on the Balance Sheet and a Debtor if otherwise.

It is liability.

The input VAT is usually deductible which means if you have more purchases than sales in a month or quarter or whatever VAT reporting period you have you will. Which reports are prepared monthly in Tally. This should have been better and more investor friendly with the rise of economic zone export oriented enterprise the service exporter business process outsourcing and all others in zero-rating. 100rate of vat 100rate of vat. But there is a practice that on the taxable purchases where input is not available they will charge entire amount including tax as purchase value. In the above entry the input VAT is more than the output VAT so the difference is Creditable input Vat.

Which reports are prepared monthly in Tally. For most of the VAT registered businesses it will always be a Creditor unless they sell exempt or zero rated products in which case their input VAT may exceed the Output VAT giving rise to a Debtor. Why Input Tax is an Asset. Including vat in your PL will make it very tricky to see what your real profits are and complicate any. Hence VAT should be shown in the books of account under a separate liability account which is ultimately reflected in the balance sheet under creditors. The total of the VAT amount column gives you the amount of Out put tax. In the above entry the input VAT is more than the output VAT so the difference is Creditable input Vat. The ending balance on the credit side of tax and surcharge payable-output VAT to be recognised should be reported under the items of other current liabilities or other non-current liabilities on the Balance Sheet when necessary. The output VAT is 30000. Some of them will give separate disclosure as purchases and tax on purchases and give a ne.

If you are buying or selling the Good which are under VAT you have to. Including vat in your PL will make it very tricky to see what your real profits are and complicate any. Profit Loss AC. The amount of Input VAT is deducted from Output VAT to determine VAT payableClaimable. Or in other words input VAT is found on supplier invoices that you receive when you have purchased something to your company. Rhodam Posted February 14 2012. Input VAT P1200000. Which reports are prepared monthly in Tally. The Balance Sheet when necessary. This input VAT expense rule had been alive for quite some time and gave taxpayers a tax benefit to the extent of reduction from income tax brought about by the input VAT expense.

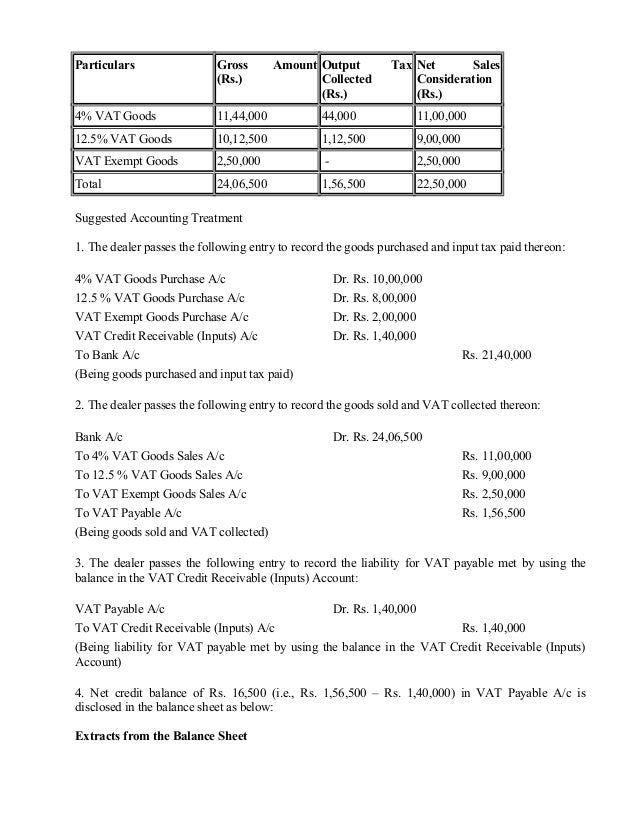

This input VAT expense rule had been alive for quite some time and gave taxpayers a tax benefit to the extent of reduction from income tax brought about by the input VAT expense. Output Tax Balance 200 Dr. On sale it will be VAT Output. This should have been better and more investor friendly with the rise of economic zone export oriented enterprise the service exporter business process outsourcing and all others in zero-rating. If you are buying or selling the Good which are under VAT you have to. VAT on Sales and Purchases can be adjusted against each other and if VAT on Purchase is more than VAT on sales during that month it will appear as Input VAT Credit under Current Assets Loans Advances if VAT on Sales is more than VAT on Purchases it will appear as VAT Payable under Current Liabilities Provisions in the Balance Sheet. The debit balance in VAT Credit Receivable Inputs Account at the year-end should be shown on the Assets side of the balance sheet under the head Loans and Advances. Cash Flow of Funds Flow. The amount of Input VAT is deducted from Output VAT to determine VAT payableClaimable. And When you add VAT to your sales purchases expenditure and fixed assets the calculated VAT figure must be inserted in the VAT line of the balance sheet to ensure that the double entry is completed.

Like any other outward payment VAT is. During the same period the business sells good worth 150000 excluding VAT with a 20 VAT rate. At the end of every VAT period if the Output VAT will exceed the Input VAT there will be creditor on the Balance Sheet and a Debtor if otherwise. Cash Flow of Funds Flow. VAT is not added to any of the numbers included in the profit and loss account. On the VAT return the 12400 input VAT should be deducted from the 30000 output VAT which in this case amounts to 17600 VAT due to HMRC. Before this sale tax was collected. Or in other words input VAT is found on supplier invoices that you receive when you have purchased something to your company. The output VAT is 30000. Some of them will give separate disclosure as purchases and tax on purchases and give a ne.

Vat MRP QTY100. In the pl you are better off keeping everything net the vat is a separate issue and balance sheet asset liability items and belongs to HMRC not the company. For most of the VAT registered businesses it will always be a Creditor unless they sell exempt or zero rated products in which case their input VAT may exceed the Output VAT giving rise to a Debtor. Required to record the adjustment ie VAT Credit Receivable Inputs Account should be credited with a corresponding debit to the account maintained for tax payable on sales. Hence VAT should be shown in the books of account under a separate liability account which is ultimately reflected in the balance sheet under creditors. Compute in put tax from purchases made during the period get it from purchase invoices and compute the total Input VAT. And When you add VAT to your sales purchases expenditure and fixed assets the calculated VAT figure must be inserted in the VAT line of the balance sheet to ensure that the double entry is completed. Cash Flow of Funds Flow. I am finalizing the accounts of a company to whom at the end of the financial year HMRC was owing tax. On purchase it will be VAT input.