Simple Financial Assets At Fair Value Through Profit And Loss Accounting For Realized Unrealized Gains Losses

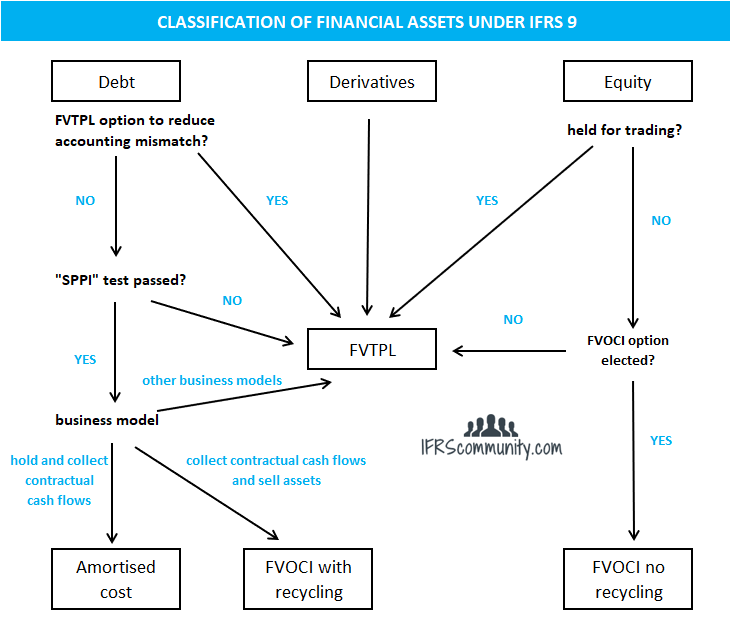

Classification Of Financial Assets Liabilities Ifrs 9 Ifrscommunity Com

In detail these investments were mainly allocated in the life segment 70341 million which accounted for 965 of this category whereas the residual part referred to the non-life segment 681 million which accounted for 0. Fair Value through Profit or Loss The FVPL accounting treatment is used for all financial instruments that are intended to be held for sale and NOT to maintain ownership. It is a valuation method that is particularly used to value financial instruments. When an entity becomes a party to a forward contract the fair values of the right and obligation are often equal so that the net fair value. Financial assets held at fair value through profit or loss comprise assets held for trading and those financial assets designated as being held at fair value through profit or loss. Under IFRS 9 all financial instruments are initially measured at fair value plus or minus in the case of a financial asset or financial liability not at fair value through profit or loss transaction costs. IFRS 9 requires changes in fair value on financial liabilities designated as at FVTPL to be split into. For the assets classified as fair value through profit or loss all gains or losses recognised in profit or loss hereinafter referred to as the profit and loss account will be taxed or allowed as a deduction even though they are unrealised. Financial fixed assets at fair value through profit or loss In addition a portfolio of financial assets that is managed and whose performance is evaluated on a fair value basis is neither held to collect contractual cash flows nor held both to collect contractual cash flows and to sell financial assets. These types of assets have a value that is constantly in flux as a result of changes in the market.

ZChanges in the fair value of available for sale assets are recognised directly in equity.

These include financial assets that an entity holds for trading purposes or are recognized at fair value through profit or loss. These types of assets have a value that is constantly in flux as a result of changes in the market. Under IFRS 9 the default financial asset measurement category is fair value through profit or loss FVTPL while under IAS 39 it is available for sale which also requires measurement at fair value but results in less volatility in profit or loss because fair value changes are recognised in other comprehensive income. Fair value through profit or loss or available for sale categories. For certain loans and advances and debt securities with fixed rates of interest interest rate swaps have. In this case the cost method is used.

Financial fixed assets at fair value through profit or loss In addition a portfolio of financial assets that is managed and whose performance is evaluated on a fair value basis is neither held to collect contractual cash flows nor held both to collect contractual cash flows and to sell financial assets. This category accounted for 176 of total investments. 15 rows financial assets measured at fair value through profit and loss showing separately those held for trading and those designated at initial recognition. Gains and losses on Financial assets at fair value through profit or loss are immediately booked to the Income Statement. When these assets are being held they are always recorded at fair value on the balance sheet and any changes in the fair value are recorded through the income statement eventually affecting net income and not other. Under IFRS 9 all financial instruments are initially measured at fair value plus or minus in the case of a financial asset or financial liability not at fair value through profit or loss transaction costs. Financial Asset at Fair Value through Profit or Loss. Fair value through profit or lossany financial assets that are not held in one of the two business models mentioned are. These include financial assets that an entity holds for trading purposes or are recognized at fair value through profit or loss. Fair value through profit or loss is a way of establishing the value of assets and liabilities on a balance sheet.

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market other than held for trading or designated on initial recognition as assets at fair value through profit or loss or as available-for-sale. For certain loans and advances and debt securities with fixed rates of interest interest rate swaps have. In detail these investments were mainly allocated in the life segment 70341 million which accounted for 965 of this category whereas the residual part referred to the non-life segment 681 million which accounted for 0. ZChanges in the fair value of available for sale assets are recognised directly in equity. For the assets classified as fair value through profit or loss all gains or losses recognised in profit or loss hereinafter referred to as the profit and loss account will be taxed or allowed as a deduction even though they are unrealised. ZLoans and receivables and held to maturity financial assets are measured at amortised cost. Gains and losses on fair valuation are recorded in the statement of profit or loss. Financial Asset at Fair Value through Profit or Loss. Financial asset at fair value through profit or loss FVTPL is subsequently measured at fair value. Fair value through other comprehensive incomefinancial assets are classified and measured at fair value through other comprehensive income if they are held in a business model whose objective is achieved by both collecting contractual cash flows and selling financial assets.

Fair value through other comprehensive incomefinancial assets are classified and measured at fair value through other comprehensive income if they are held in a business model whose objective is achieved by both collecting contractual cash flows and selling financial assets. Under IFRS 9 all financial instruments are initially measured at fair value plus or minus in the case of a financial asset or financial liability not at fair value through profit or loss transaction costs. Financial Assets and Liabilities at Fair Value through Profit or Loss A financial asset is held for trading if acquired or originated principally for the purpose of generating a profit from short-term fluctuations in price or if it is part of a portfolio of identified instruments that are managed together and for which there is intention of short-term profit-taking. IFRS 9 requires changes in fair value on financial liabilities designated as at FVTPL to be split into. Financial asset at fair value through profit or loss FVTPL is subsequently measured at fair value. ZLoans and receivables and held to maturity financial assets are measured at amortised cost. As measured at fair value through profit or loss refer note 2 below Net fair value is recognised as an asset or a liability on the commitment date Forward contract On the commitment date. Journal Entries for Financial Assets and Financial Liabilities held at Fair Value Through Profit or Loss FVTPL under IFRS 9. These types of assets have a value that is constantly in flux as a result of changes in the market. In this case the cost method is used.

For the assets classified as fair value through profit or loss all gains or losses recognised in profit or loss hereinafter referred to as the profit and loss account will be taxed or allowed as a deduction even though they are unrealised. This requirement is consistent with IAS 39. In detail these investments were mainly allocated in the life segment 70341 million which accounted for 965 of this category whereas the residual part referred to the non-life segment 681 million which accounted for 0. Fair value through profit or lossany financial assets that are not held in one of the two business models mentioned are. Financial Asset at Fair Value through Profit or Loss. As measured at fair value through profit or loss refer note 2 below Net fair value is recognised as an asset or a liability on the commitment date Forward contract On the commitment date. Available-for-sale financial assets are measured at fair value unless a market price or fair value cannot be reliably determined. Financial assets held at fair value through profit and loss. Financial assets held at fair value through profit or loss comprise assets held for trading and those financial assets designated as being held at fair value through profit or loss. Fair value through other comprehensive incomefinancial assets are classified and measured at fair value through other comprehensive income if they are held in a business model whose objective is achieved by both collecting contractual cash flows and selling financial assets.

This category accounted for 176 of total investments. Under IFRS 9 the default financial asset measurement category is fair value through profit or loss FVTPL while under IAS 39 it is available for sale which also requires measurement at fair value but results in less volatility in profit or loss because fair value changes are recognised in other comprehensive income. In detail these investments were mainly allocated in the life segment 70341 million which accounted for 965 of this category whereas the residual part referred to the non-life segment 681 million which accounted for 0. Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market other than held for trading or designated on initial recognition as assets at fair value through profit or loss or as available-for-sale. IFRS 9 requires changes in fair value on financial liabilities designated as at FVTPL to be split into. Financial Asset at Fair Value through Profit or Loss. It is a valuation method that is particularly used to value financial instruments. Gains and losses on fair valuation are recorded in the statement of profit or loss. Financial Assets and Liabilities at Fair Value through Profit or Loss A financial asset is held for trading if acquired or originated principally for the purpose of generating a profit from short-term fluctuations in price or if it is part of a portfolio of identified instruments that are managed together and for which there is intention of short-term profit-taking. ZLoans and receivables and held to maturity financial assets are measured at amortised cost.